There are few who would question the need to deliver more homes. Research from Centre for Cities suggests Britain has a 4.3 million home deficit compared with the average European country. Meaning we would need to build almost 450,000 homes per annum over the next 25 years to satisfy future demand and address the historic deficit. At present we struggle to hit 200,000.

But for those looking to deliver new homes, higher debt costs, more legislative hoops, and planning delays, are all deterring activity. The number of housing projects granted planning permission in Q2 2023 fell 10% on Q1 and was down 20% on volumes a year ago, according to figures from the HBF. Just over 135,000 homes were approved in the first half of 2023, 17% fewer than during the same period a year ago. In London, Molior reported that the number of units granted permission across the capital in Q2 2023 was at the lowest level for 11 years. All of which raises the likelihood of stock scarcity as fewer schemes progress through the planning process and start on site.

The economy

UK GDP figures show the economy contracted by -0.5% in July, higher than the forecasts of a -0.2% fall and down from +0.5% in June. Recent fluctuations have taught us not to read too much into monthly figures, particularly as July’s inclement weather and days lost to industrial action could well be behind the higher than anticipated fall in GDP. But even so, the disappointing GDP figures have re-ignited fears of a recession, it does not take much….

But revised figures on UK GDP have changed the economic narrative we have become familiar with over the last two years. Revisions to the 2020 and 2021 growth figures show the UK recovered to its pre-pandemic peak in Q4 2021. Before figures were revised the size of the UK economy was -1.2% smaller than the pre-pandemic peak in Q4 2021 compared to a revised +0.6%.

These new numbers mean the UK, which had been seen as very much the laggard of the G7, was instead firmly in the middle of the pack. The recovery behind the likes of Canada and the USA, but faster than Germany, Italy, and Japan.

The job market

Wage growth including bonuses reached an inflation busting 8.5% in the three months to July. With one off bonus payments pushing public sector pay up by more than 12%. This is the first-time wages have risen by more than inflation for two years.

Wage growth now higher than inflation but rents outpace both

Alongside working households, this is welcome news for those receiving state pensions. With the triple lock meaning pensions look set to rise 8.5% in April, if one-off public-sector bonuses are not stripped out of the figures as some ministers have suggested. Either way a costly increase for the government in the run up to the Autumn statement.

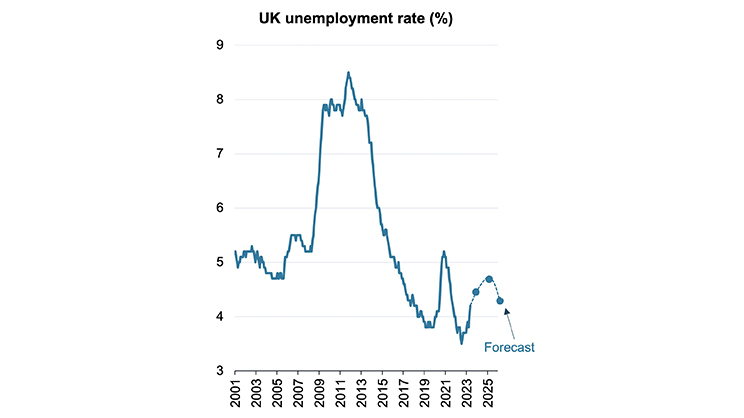

Wage growth has been fuelled, at least in part, by a competitive employment market. Back in May 2022 job vacancies hit an all time high of 1.3 million, with the unemployment rate hitting a low of 3.5% last summer. Rates have been rising since, with the total number of people employed falling by more than 200,000 in the three months to July, and the unemployment rate rising to 4.3%. But it remains low in a historic context and broadly in line with forecasters expectations.

Labour markets loosen a little but remain in good health

Unemployment is still low and wages are rising

Sales

The European Central Bank increased the deposit rate from 3.75% to 4% on 14 September, the highest rate since the inception of the Euro in 1999. We will not know until 21 September whether the Bank of England will follow suit, but the prospect of a further rise in the bank rate appears to already be priced in to fixed rates. Some lenders announcing further small reductions in fixed rates in recent weeks. But uncertainty over rates continues to impact levels of activity across the market. Bank of England figures show gross mortgage advances in Q2 2023 totalled £52.4 billion, almost a third down on the same three months a year ago.

In some ways the RICS July report made for quite sobering reading. With respondents reporting fewer sales and lower levels of demand over the summer. But equally there appears to be little sign of distress, with potential home movers waiting to see where rates settle, with inventory on agents books holding steady and remaining lower than long run averages.

Rents

The latest RICS survey reported further increases in tenant demand in the three months to July. With a net balance of +54% of respondents reporting a rise in demand. The strongest three-monthly pick-up in demand since the start of 2022. With this back drop it will not be much of a surprise that most respondents expected rents would rise over the coming three months, the +63% balance marking a record high.

But figures from Zoopla suggest an easing of the acute supply demand imbalance in the rental market. The number of homes available to let up 20% on the same point a year ago, but still 30% below the long run average. A year ago, rental growth hit 12.1% according to Zoopla, it has eased back a little this year to 10.5%, but the double digit increases still outstrip growth in incomes. Rising rents meaning tenants pay an average of £2,772 per year more than they did three years ago.